.png?w=128&h=128&auto=format)

.png?w=256&h=256&auto=format)

.png?w=128&h=128&auto=format)

.png?rect=0,205,1614,1211&w=1600&h=1200&fit=min&auto=format)

Aye Finance: Unlocking Credit for India's Micro-Enterprises

Congrats to Sanjay and the entire Aye Finance team on the IPO!

Aye Finance: Unlocking Credit for India's Micro-Enterprises

Congrats to Sanjay and the entire Aye Finance team on the IPO!

Team Aye Finance at the listing ceremony on February 16, 2026

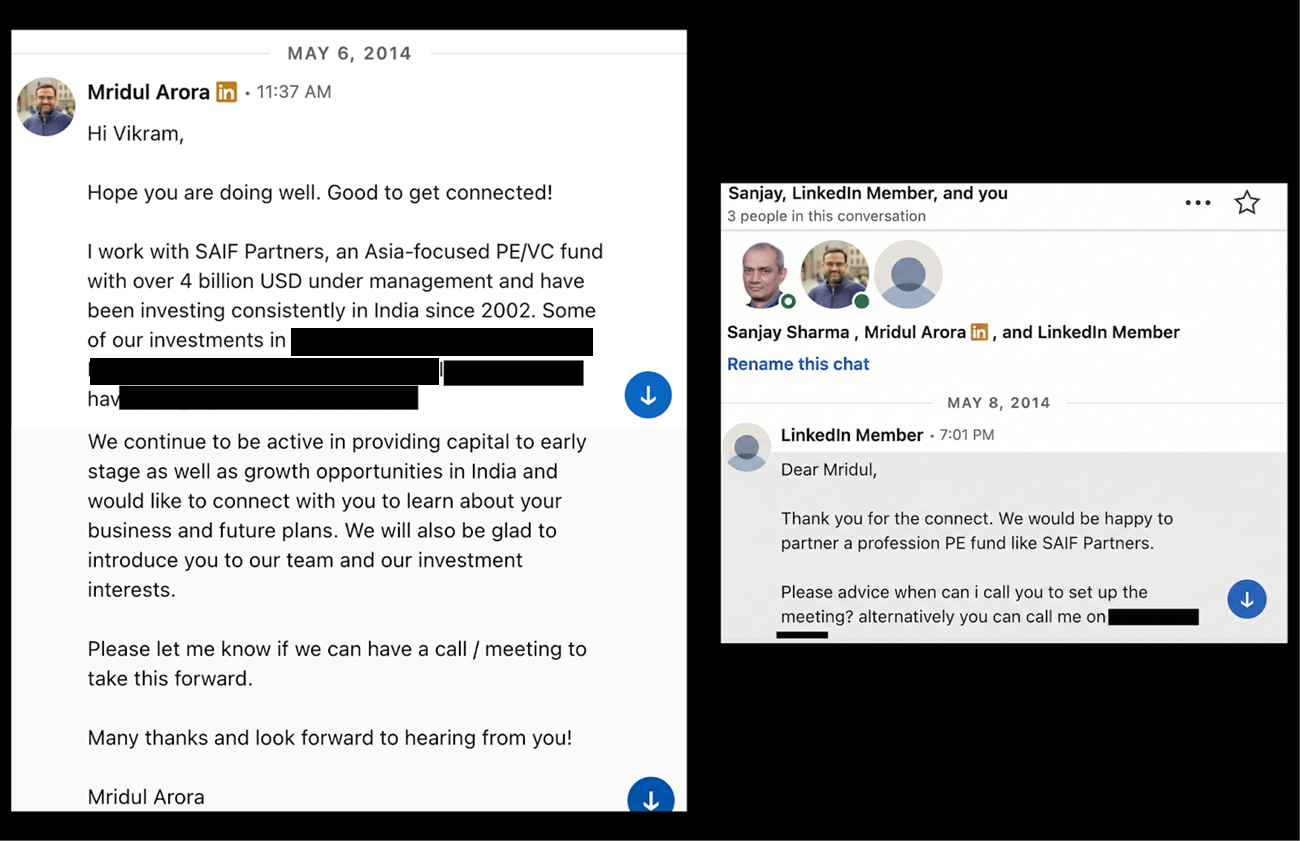

We've always believed that the best partnerships don't happen by waiting for deals to arrive - they happen by actively seeking out founders building something meaningful. On May 6, 2014, we sent a LinkedIn message to the co-founders of a months-old NBFC that had just made its first loans. It was a cold outreach - the kind we send to dozens of founders each year, hoping to start a conversation.

That exchange set in motion an eleven-year journey that brings us here today.

.png?w=1200&h=776&auto=format)

In late 2014, we sat across from Sanjay Sharma (and erstwhile co-founder Vikram Jetley) in a small office in Delhi). On paper, we were meeting the founders of a six-month-old NBFC with two branches, 126 customers, and a loan book of Rs. 1.25 crores. In practice, we were meeting a career banker; Sanjay had spent 25 years building consumer banking businesses across HSBC, HDFC Bank, ICICI, Ujjivan and Standard Chartered. He had been CEO of a housing finance company in the UAE that grew to a $3 billion portfolio. Sanjay returned to India with plans to start a school for underprivileged children. Instead, after a year working at a leading microfinance institution, he identified a gap that no one was addressing: the 6.4 crore micro-enterprises that formed the backbone of India's informal economy but had zero access to formal credit.

Shoe manufacturers in Agra. Cricket ball makers in Meerut. Lock and brass workers in Aligarh. Garment units in Delhi. These were businesses - with employees, inventory, customers, and ambitions - that needed working capital to grow. And they were completely invisible to the banking system.

Before making a single loan, Sanjay and his team had spent months conducting primary research across six industry clusters, interviewing 350 micro-entrepreneurs, mapping everything from their working capital cycles to their borrowing patterns to their willingness to repay. They were building a thesis from the ground up.

In March 2014, Aye Finance made its first loan: Rs. 1.25 lakhs to a women's shoe manufacturer in West Delhi who employed six people and produced 200 pairs a week. She had never accessed formal credit in her life. Banks wouldn't look at her, moneylenders would charge her 60-80% annually. Aye offered her capital at a transparent rate, with a one-week turnaround.

That single loan contained the entire thesis: India's micro-enterprises weren't inherently risky. They were simply invisible to a financial system built for a different kind of borrower.

When we invested in December 2014, we were cognizant that we were entering a balance sheet business very early in its life - one that would take much longer to scale and potentially IPO than typical technology investments. It has been eleven. And watching Aye go public today, we can say with certainty: it was worth every year.

The Cluster Insight

The fundamental problem Aye set out to solve was not just access to capital - it was the absence of a credit assessment model for customers who had no formal documentation. Traditional underwriting required bank statements, ITR filings, audited financials, and credit bureau scores. Micro-enterprises had none of these. So banks refused to lend, and micro-entrepreneurs were left with no choice but informal lending.

Aye’s insight was deceptively simple: if you understand the economics of a business cluster deeply enough, you can estimate income without traditional documents.

Consider a shoe manufacturer in Agra. Every shoe manufacturer in that cluster operates within similar constraints - similar raw material costs, similar labor rates, similar margins, similar cash conversion cycles. If you know the number of workers, the electricity bill, the size of the workspace, and the inventory on hand, you can arrive at a reliable estimate of monthly revenue. The shoemaker may not have a P&L statement, but the P&L exists - it's embedded in the observable characteristics of the business.

This was the genesis of Aye's cluster-based underwriting approach. Rather than asking borrowers to produce documents they didn't have, Aye's team went into the field to understand what made each cluster tick. They mapped asset turnover ratios, margin structures, peak and off-peak seasons, supply chain dynamics. They built credit frameworks for shoe-making, then sports goods, then lock and brass hardware, then garments, then carpets, then glasswork, then dairy - cluster by cluster, geography by geography. Today, Aye serves over 100 clusters across 300+ branches in 20 states.

Resilience Forged in Fire

In November 2016, less than three years into Aye's journey, the Government of India announced demonetization. For Aye's customers - micro-enterprises that transacted almost exclusively in cash - this was an existential shock. Business came to a standstill. There was no cash to pay workers, no cash to buy raw materials, no cash to receive from customers.

If any borrower segment was going to default en masse, it should have been this one.

What happened instead became a proof point that has defined Aye's story ever since. Gross NPAs, understandably, increased but remained largely range-bound. In the middle of the most severe liquidity shock India's informal economy had ever faced, Aye's customers demonstrated a proof-point of the core thesis: they had intent to repay, and they would find a way.

Then came GST implementation in 2017, which created widespread fear that informal businesses without GST registration would be shut out of the economy. Again, the portfolio held.

And then came COVID-19 in 2020 - a once-in-a-century disruption that halted economic activity nationwide. For weeks, Aye couldn't even send loan officers into the field. At the worst point, gross NPAs touched 7.7%. But by the end of the fiscal year, they had recovered to 3.5%.

What these stress tests revealed was the fundamental strength of Aye's customer base and underwriting model. These weren't borrowers who disappeared at the first sign of trouble. They were business owners with years of operating history, deep community roots, and a strong desire to maintain their creditworthiness.

The Phygital Path

One of the defining choices Aye made early on was to reject the purely digital path.

By the mid-2010s, the fintech revolution was in full swing. The dominant narrative was that technology could eliminate the need for physical infrastructure - that lending could be done entirely through apps and algorithms. For many customer segments, this was true. But for micro-enterprises in Aligarh and Agra, it was not.

Reaching them required physical presence - a loan officer who could walk into their workshop, understand their business, and guide them through the process.

But Aye didn't stop at physical presence. What they built was a "phygital" model: high-touch customer acquisition combined with tech-enabled back-end processing. The loan officer goes to the customer, but from that point forward, everything is digital - paperless applications, electronic KYC, centralized underwriting, automated collections.

This was harder to build than either a pure-play digital lender or a traditional branch-based NBFC. It required investment in both field infrastructure and technology platforms. It required training thousands of loan officers to use mobile applications effectively. It required building data science capabilities to continuously improve credit models.

And the efficacy of the model shows up in productivity: Aye's loan officers disburse approximately 6 loans per month, compared to 1.5-2 at comparable finance companies.

Founder's Second Act

Sanjay Sharma's journey is, in many ways, the opposite of the typical startup founder story.

He didn't start young. He started at 50+, after a full career in blue-chip financial institutions. He didn't start because he had to - he started because he wanted to create impact. He didn't start with a quick win in mind - he started knowing this would take a decade or more.

What Sanjay brought to Aye was not just credibility but mastery. He had spent his career understanding how financial institutions work - how to build credit processes, how to manage operations, how to attract capital, how to navigate regulation. When he turned that expertise toward micro-enterprise lending, he brought a rigor that most early-stage startups lack.

He also brought patience. From the beginning, Aye was built as an institution, not a startup looking for a quick flip. The early years were spent laying foundations - cluster by cluster, branch by branch, process by process. There was no growth-at-all-costs phase. There was just steady, compounding progress.

Alongside Sanjay, erstwhile co-founder Vikram Jetley brought deep operational expertise from his years in banking and microfinance. Together, they assembled a team of senior professionals from across the industry - people who could have worked anywhere but chose to be part of this mission.

Watching Sanjay's journey over the last eleven years has been one of the privileges of this partnership.

The Mission Continues

Today, Aye has disbursed over Rs. 10,000 crores in loans. They have served over 8.5 lakh micro-enterprises across the country - shoe makers, garment manufacturers, dairy farmers, restaurant owners, grocery stores, beauty parlors. Each of those businesses employs an average of four people. Each of those people supports a family.

For many of these borrowers, Aye was their first experience with formal credit. The loan repayment data Aye reports to credit bureaus is creating credit histories where none existed before. The businesses that access capital are growing - hiring more workers, buying more equipment, serving more customers. The virtuous cycle of formalization is underway.

The market remains vast. There are still 6+ crore micro-enterprises in India, and the penetration of formal credit remains low. The need Aye identified in 2014 is as acute as ever.

As Aye goes public today, we feel immense pride in what the team has built. Not just the scale - though the scale is remarkable - but the choices that created it: the conviction to serve customers everyone else ignored, the patience to build cluster expertise over a decade, the resilience to navigate crises that would have broken a lesser institution.

Thank you, Sanjay, Vikram, and every member of the Aye Finance team, for letting us be part of this journey. It has been a privilege.

The IPO is only a milestone, as the mission is still just getting started.

Written by Mridul Arora

Related

Harnessing Better Experience And Innovative GTM: Marketplaces Unleashed Part 3

Exploring the last two pillars of our marketplaces framework through case studies

03.08.2023

Vridhi: Reimagining Home Lending For Bharat's Self-Employed

Ram Naresh Sunku, Co-founder, Vridhi Home Finance

11.12.2024

Investing in Atlys

Building the world’s largest digital visa provider

21.09.2023